The deductibility of expenses funded with Paycheck Protection Program (PPP) loans is one of the most beneficial provisions of the Consolidated Appropriations Act, 2021. Add to this benefit the tax-exempt nature of PPP funds, and the loan program delivers the full level of federal relief intended in the CARES Act.

But does this mean all borrowers will completely avoid taxation of loan proceeds and deductibility of PPP-funded expenses? The answer depends on the state(s) in which they operate.

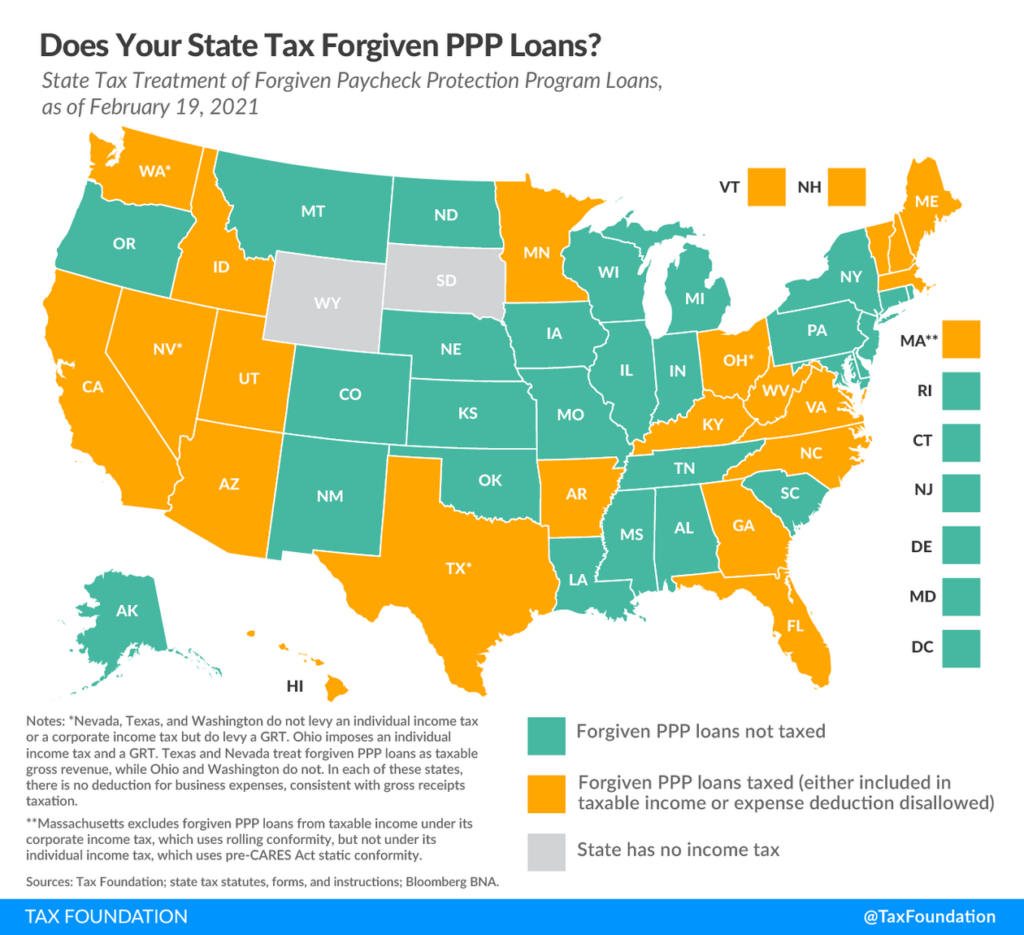

States have been announcing their positions on the tax treatment of PPP loans and whether they will conform to federal law in whole, in part, or not at all.

Nearly half the states have decided to tax forgivable PPP income, as evidenced in the map below.

State Highlights

New York, New Jersey and Connecticut are three of the 27 states that have announced they will conform to federal law on both the non-taxability of forgiven PPPs loans and the deductibility of PPP-funded expenses.

Massachusetts is taking a unique position that the taxability will apply only to individuals. Corporate taxpayers will not be taxed on their PPP loans but cannot deduct expenses that are paid for with forgiven funds.

Some states, like California and North Carolina, are “meeting taxpayers halfway” as they allow the non-taxability of PPP funds but not the deductibility of forgiven expenses. Minnesota and New Hampshire took the opposite stance, allowing the deductibility but taxing the PPP funds. Wisconsin chose yet another approach, announcing it will not tax first draw PPP loans but will tax second draw loans.

One thing is clear – the treatment of PPP loan funds will vary widely by state. All of this makes a confusing situation even more so. This is especially true for businesses that operate in more than one state. It is imperative that taxpayers who received PPP loans work with knowledgeable tax professionals like Grassi’s to make the correct reporting of PPP loan forgiveness and PPP funded expenses.

If you have any questions about the tax treatment of your PPP funds or other state and local tax issues, please contact your Grassi tax advisor.